Aerospace And Defense Additive Manufacturing Global Market Opportunities And Strategies To 2035

By Technology (Direct Metal Laser Sintering (DMLS), Fused Deposition Modeling (FDM), Continuous Liquid Interface Production (CLIP), Stereolithography (SLA), Selective Laser Sintering (SLS), Other Technologies), By Material (Metal, Plastic, Rubber, Other Materials), By Platform (Aviation, Defense, Space), By Application (Engine Component, Space Component, Structural Component, Defense Equipment, Other Application), And By Region, Opportunities And Strategies – Global Forecast To 2035

Aerospace And Defense Additive Manufacturing Market Definition

Aerospace and defense additive manufacturing refers to the application of layer-by-layer fabrication technologies — commonly known as 3D printing — to produce components, tooling, prototypes and end-use parts for the aerospace and defense sectors. These technologies encompass a range of processes including direct metal laser sintering (DMLS), selective laser sintering (SLS), fused deposition modeling (FDM), stereolithography (SLA), continuous liquid interface production (CLIP) and electron beam melting (EBM), each suited to different materials and performance requirements. The aerospace and defense additive manufacturing market consists of revenues from the sale of additive manufacturing hardware, materials (metals, polymers, rubber and composites), software and related services used for the fabrication of aerospace and defense components. Key applications include engine components, space components, structural components, defense equipment and related sub-assemblies. End users encompass commercial aircraft OEMs, military aircraft manufacturers, satellite and launch vehicle producers, defense contractors and MRO (maintenance, repair and overhaul) service providers.

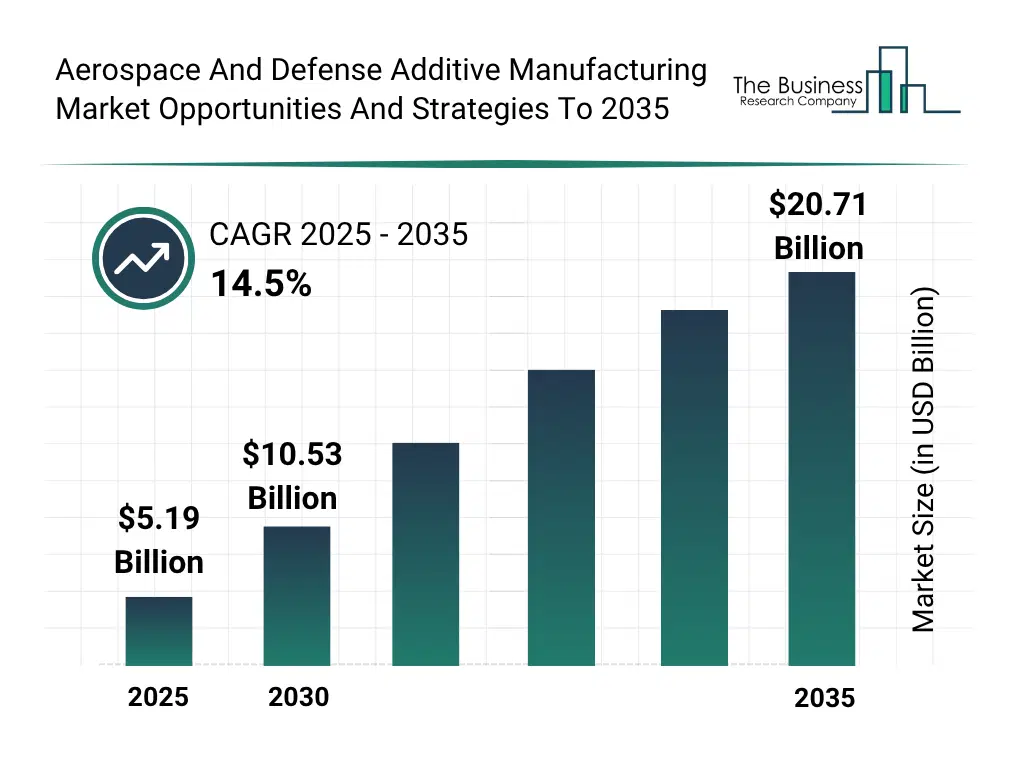

Aerospace And Defense Additive Manufacturing Market Size

The global aerospace and defense additive manufacturing market reached a value of nearly $5,194.3 million in 2025, having grown at a compound annual growth rate (CAGR) of 15.7% since 2020. The market is expected to grow from $5,194.3 million in 2025 to $10,529.3 million in 2030 at a rate of 15.2%. The market is then expected to grow at a CAGR of 14.5% from 2030 and reach $20,709.2 million in 2035. Growth in the historic period resulted from increasing aircraft orders worldwide, increasing demand for lightweight and fuel-efficient aerospace components, growth of unmanned aerial vehicles and autonomous defense systems and government and defense investments in additive manufacturing techniques. Factors that negatively affected growth in the historic period were high initial capital costs and material limitations and qualification issues. Going forward, growth in space and advanced aviation programs, increased adoption of additive manufacturing in hypersonic programs, growth of defense modernization programs and growth in aerospace maintenance, repair and overhaul (MRO) activities will drive the growth. Factors that could hinder the growth of the aerospace and defense additive manufacturing market in the future include stringent certification requirements, lack of skilled workforce with aerospace additive manufacturing and impact of trade war and tariff.

Aerospace And Defense Additive Manufacturing Market Segmentation

The aerospace and defense additive manufacturing market is segmented by technology, by material, by platform and by application.By Technology –

The aerospace and defense additive manufacturing market is segmented by technology into:

- a) Direct Metal Laser Sintering (DMLS)

- b) Fused Deposition Modeling (FDM)

- c) Continuous Liquid Interface Production (CLIP)

- d) Stereolithography (SLA)

- e) Selective Laser Sintering (SLS)

- f) Other Technologies

By Material –

The aerospace and defense additive manufacturing market is segmented by material into:

- a) Metal

- b) Plastic

- c) Rubber

- d) Other Materials

By Platform –

The aerospace and defense additive manufacturing market is segmented by platform into:

- a) Aviation

- b) Defense

- c) Space

By Application –

The aerospace and defense additive manufacturing market is segmented by application into:

- a) Fixed-Wing Drone

- b) Rotary Wing Drone

- c) Hybrid Wing Drone

By End User –

The aerospace and defense additive manufacturing market is segmented by end user into:

- a) Engine Component

- b) Space Component

- c) Structural Component

- d) Defense Equipment

- e) Other Application

By Geography - The aerospace and defense additive manufacturing market is segmented by geography into:

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- USA

- Canada

- Brazil

- France

- Germany

- UK

- Italy

- Spain

- Russia

-

o Asia Pacific

o Africa